What are Principal & Interest loans?

Understanding property finance 👉6

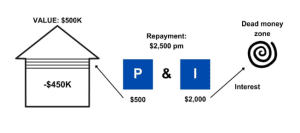

Principal and interest (P&I) loans can be broken down into two elements: the principal payment and the interest charge. The principal payment is what pays down the loan and chips away at the loan every month until your 25-year term expires and the loan is paid up in full. The interest charge is the fee the bank charges you for borrowing the money. This amount doesn’t go onto your loan, but rather straight to the bank. That’s how they make their money, by charging you interest on your loans. You could call this the ‘dead money zone’. Most people say rent money is dead money, but so is the interest you pay on your mortgage.

Let’s take the example of a property worth $500,000 with a $400,000 loan and a monthly repayment of $2,500. The principal amount of $500 reduces the loan, while the remaining $2,000 is the interest charge.

The elements of a principal and interest loan

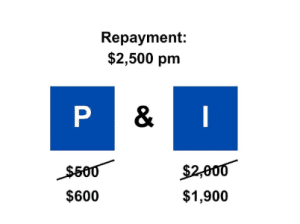

What happens over time is that your repayments stay the same, but as your loan slowly decreases, the amount of interest charged decreases too. The apportionment of your repayment on principal and interest actually changes, so your $2,500 is now divided into $1,900 for the interest and $600 towards the principal. At this point, you begin to pay your loan down faster.

Changes in P&I loan repayments over time

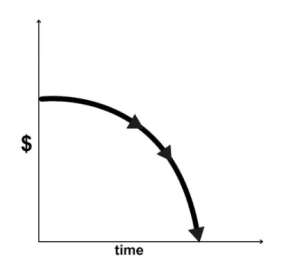

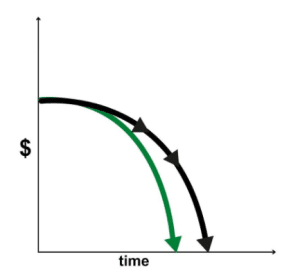

When you take out a mortgage on P&I, the loan pays down slowly in the beginning. As the principal amount reduces the loan, the interest charges become less and less over time. By this point, more money is going toward the principal and the loan will start paying itself off faster. Refer to the below figure and you’ll see that it pays off faster towards the end.

A P&I loan paying off faster with time

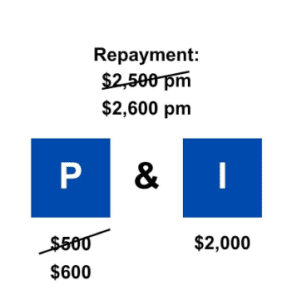

Have you heard people say: Pay an extra $100 per month on your mortgage and wipe off 5 years from the loan? It sounds a bit nonsensical, doesn’t it? How could $100 really make that much of a difference?

Let me explain: What actually happens is that the $100 is added to the $500 principal, not to the full $2,500 repayment. That works out to 20% more going on your principal and that’s what makes a big difference to your loan in the end. This is one strategy to pay your loan off faster.

Paying an additional $100 per month on a P&I loan

This strategy is great for investment properties because as the years go by and your rents rise, you’ll have extra cash to add to your principal every month. This will help you pay off an investment property even faster than your own home. If you put all of the income you earn from rent back into your mortgage, you could easily pay off the loan in 10-15 years.

Increased rate of paying off a P&I loan over time

Join me for the seventh property finance insight next.

Stay tuned for more daily insights from Wealth Through Property.

~Daimien Patterson