Why you need Interest-only (I/O) loans

Understanding property finance 👉7

Are you finding this series on “Understanding Property Finance” helpful?

Interest-only (I/O) loans are pretty simple. As the name suggests, you pay only the interest portion of the repayment and no principal. This means the amount you owe on your loan doesn’t change.

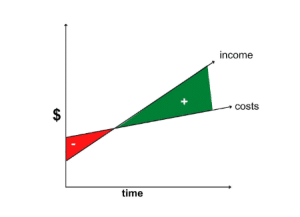

If you look at a property over time, the costs of owning the property will go up slightly with inflation. The income you receive from rent on the property will also increase, doubling every 10 years. At the start, your income might be less than your costs and you’ll have what we call a negatively-geared property. As time goes by your income will eventually exceed your costs, creating a positive cash flow and a positively-geared property.

Investment property costs vs. expenses over time

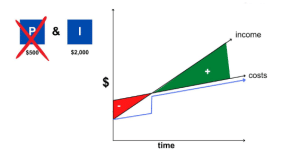

This is where I/O loans can be quite effective to deal with the negative cash flow at the start. Let’s say you have a property worth $500,000 with a loan of $400,000 and a repayment of $2,500. In order to save money and avoid having a negatively-geared property, you opt for an I/O loan and reduce your repayment to $2,000 per month.

This will drop your expenses by $500 per month in those early stages and allows the property to have a positive cash flow. (See the revised line below.)

Decreased property costs with an I/O loan

If you can, make use of an I/O loan for about the first 5 years to drop expenses so that the property can support itself. When the rent has gone up enough, convert to a P&I loan and begin making the principal payments when your property has a higher, positive cash flow.

Join me for the eighth property finance insight.

Stay tuned for more daily insights from Wealth Through Property.

~Daimien Patterson