How Are Interest Rates Set In Australia?

Understanding interest rates should be an essential part of every property investor’s (and indeed, every Australian citizen’s) education.

After all, they have a huge effect on not only an investor’s portfolio and finances, but how our country’s economy works.

How Interest Rates Used to be Set

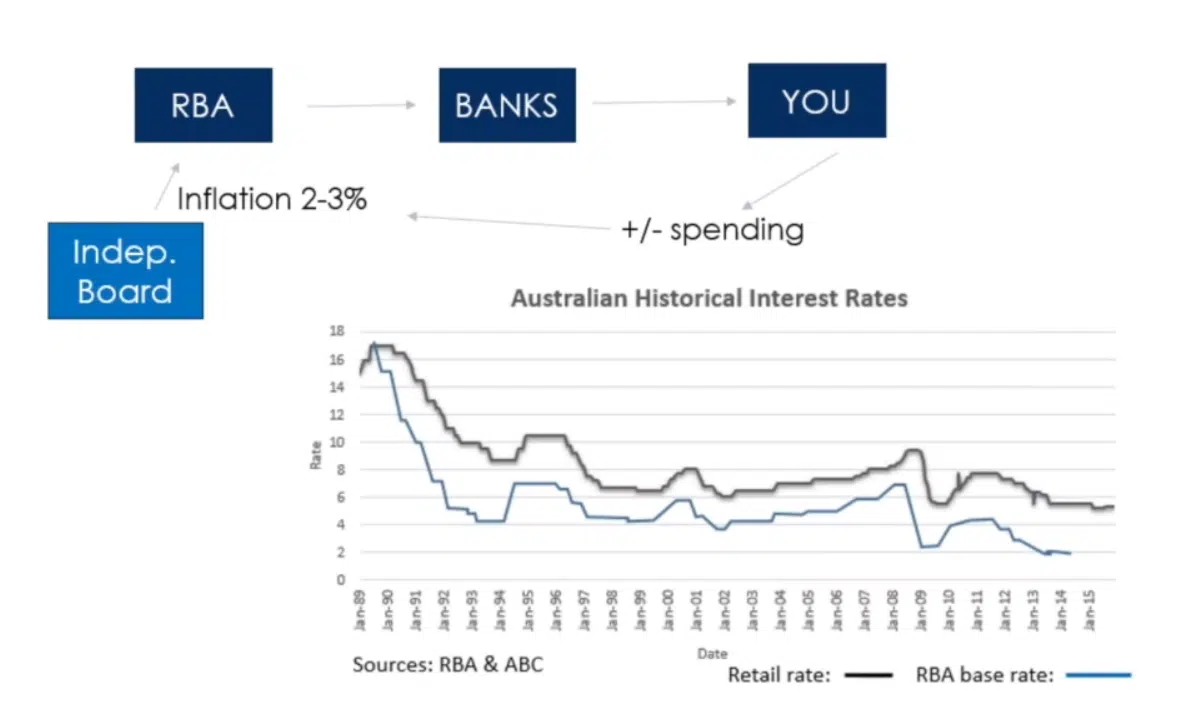

Just a couple of decades ago, interest rates were set by the government. The Reserve Bank of Australia would lend money to banks, who would then lend money to consumers. The RBA lends the money at a variable rate to banks, and the banks pass this rate on with a mark-up to make some money in the process.

The problem with public servants and the government controlling the interest rate was that they could use it to their political advantage. After all, the interest collected by the RBA is revenue for the government that is then used to pay for their expenses and promises, so parties would ramp up interest rates when they had bills to pay, which, as you can imagine, was not healthy for the economy.

How Interest Rates are Set Now

During the recession in the 90s, then Prime Minister Paul Keating decided to make the RBA independent, by setting an independent board to govern it with the following duties and goals:

- To stabilise the currency of Australia

- To help maintain employment levels

- Ensure the economic prosperity and welfare of Australians

Source: http://www.rba.gov.au/about-rba/history/

The ideal inflation rate was identified as 2-3% per year on average to ensure these targets were met. The RBA board is able to influence inflation rates by adjusting the interest rates. Here’s how…

- Each month, they check the prices of key indicators – everything from the price of milk to the price of petrol, and everything in between

- Price trends are noted to see what inflation is doing

- If it appears that inflation is going up significantly, the RBA board will put the interest rate up

- In turn, the banks will increase their lending rate, which will result in homeowners and property investors having less money to spend, which reduces pressure on inflation

- The opposite will happen if inflation is going down significantly

- The RBA will drop the interest rates, leading to banks dropping their lending rate, and anyone with a mortgage will find they have more money to spend, which will help inflation level out again

Thus, the RBA helps to stimulate or de-stimulate the economy as needed.

What GFC?

You’ll have to admit that it’s a pretty brilliant system, which is evidenced by how well we did even through the Global Financial Crisis. When the crisis hit Australia, the RBA board dropped interest rates by about 4.5% in just 6 months, a move which helped to keep the economy stable when the rest of the world was in turmoil.

I can remember when the GFC hit Australia and I had a multi-million-dollar property portfolio. Was I worried? Nope! Interest rates dropped and I certainly didn’t feel affected by any financial strife.

Historical Interest Rate Trends

I like looking at the historical basis for interest rates, and what events have caused them to go up and down. Take a look at the graph below. The blue line is the RBA’s interest rate, and the black line is the banks’ lending rate.

So, let’s talk about some of the events that correlate to the peaks and troughs we’re looking at.

1990: We were at the height of the recession with double digit interest rates. The board governing the RBA was made independent, driving the rate down to stimulate the economy.

1995-6: The economy starts to recover and the tech boom takes off. Shortly after this, the tech collapse occurs in the late 90s.

2001: September 11 terrorist attack in America, resulting in Wall Street closing for two weeks. The world was massively uncertain about the markets. America invaded the Middle East, Afghanistan, and then Iraq. As a result of this uncertainty, the RBA dropped the rate.

2002- 2008: Australia enters a time of great prosperity and interest rates go up gradually.

Oct 2008: The GFC hits, resulting in interest rates dropping from 6.5% down to 2.25% in a short amount of time.

2010-11: Things go quiet as Australia starts to recover, and is seen as one of the top investment choices around the world. Australia also gets a mining booms which further boosts the economy and interest rates go up to slow inflation.

2012: The mining boom comes to an end and interest rates fall again.

Interest Rates in 2017

So, where are interest rates at right now? We’re sitting at 1.5%, the lowest our country has ever seen, and they’re going to stay there for quite a while.

This is a GOOD opportunity for savvy property investors to get into property now, fix their rate for, say, 5 years, and hold the properties for that period, while rents go up, and then reassess at the end of the period.

Want to learn more about how property investing can secure your financial future?

Click below and gain access to a FREE webinar.

Daimien Patterson is the CEO of Integrity Property Investment, a property investment company based in Australia. He regularly produces books, blogs and videos on the topic of property investing, helping thousands of people create financial security and freedom through education and property investment. Get started today.

{kind=link}